Revenue

$2.00B

2023

Valuation

$33.00B

2023

Growth Rate (y/y)

82%

2023

Funding

$1.72B

2023

Revenue

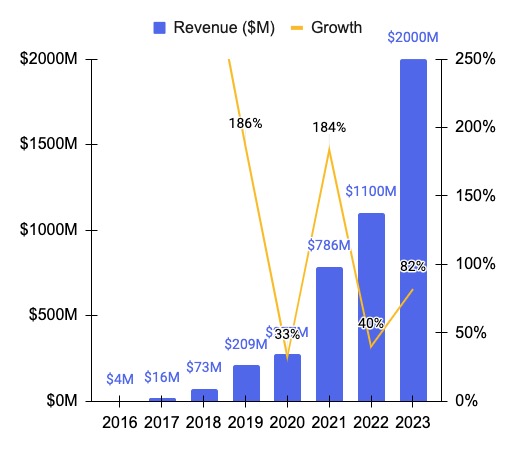

Sacra estimates that Revolut generated $2B of revenue in 2023, up about 82% from $1.1B in 2022.

Revolut previously grew 189% between 2020 and 2021, from £220M to £636M, on the back of an explosion in crypto and fintechs during COVID.

In addition, Revolut's gross margin improved from 33% to 70% from 2020 to 2021.

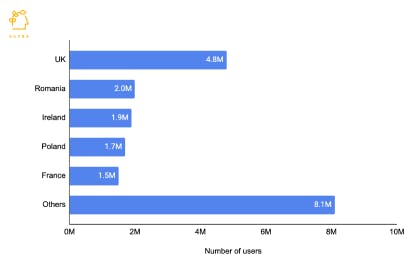

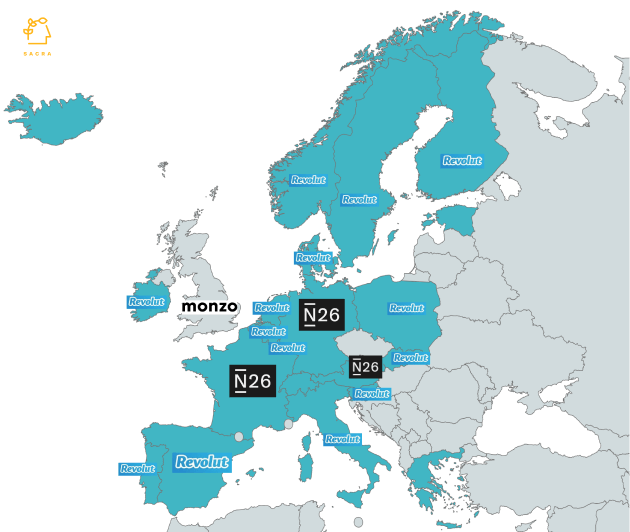

Revolut is present in 36+ countries with 27M retail and 500,000+ business customers, making it the largest neobank in Europe.

Note: Revolut's top 5 countries by users

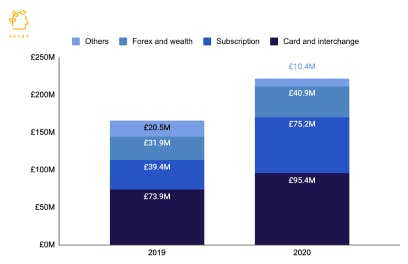

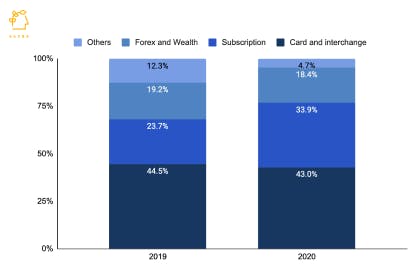

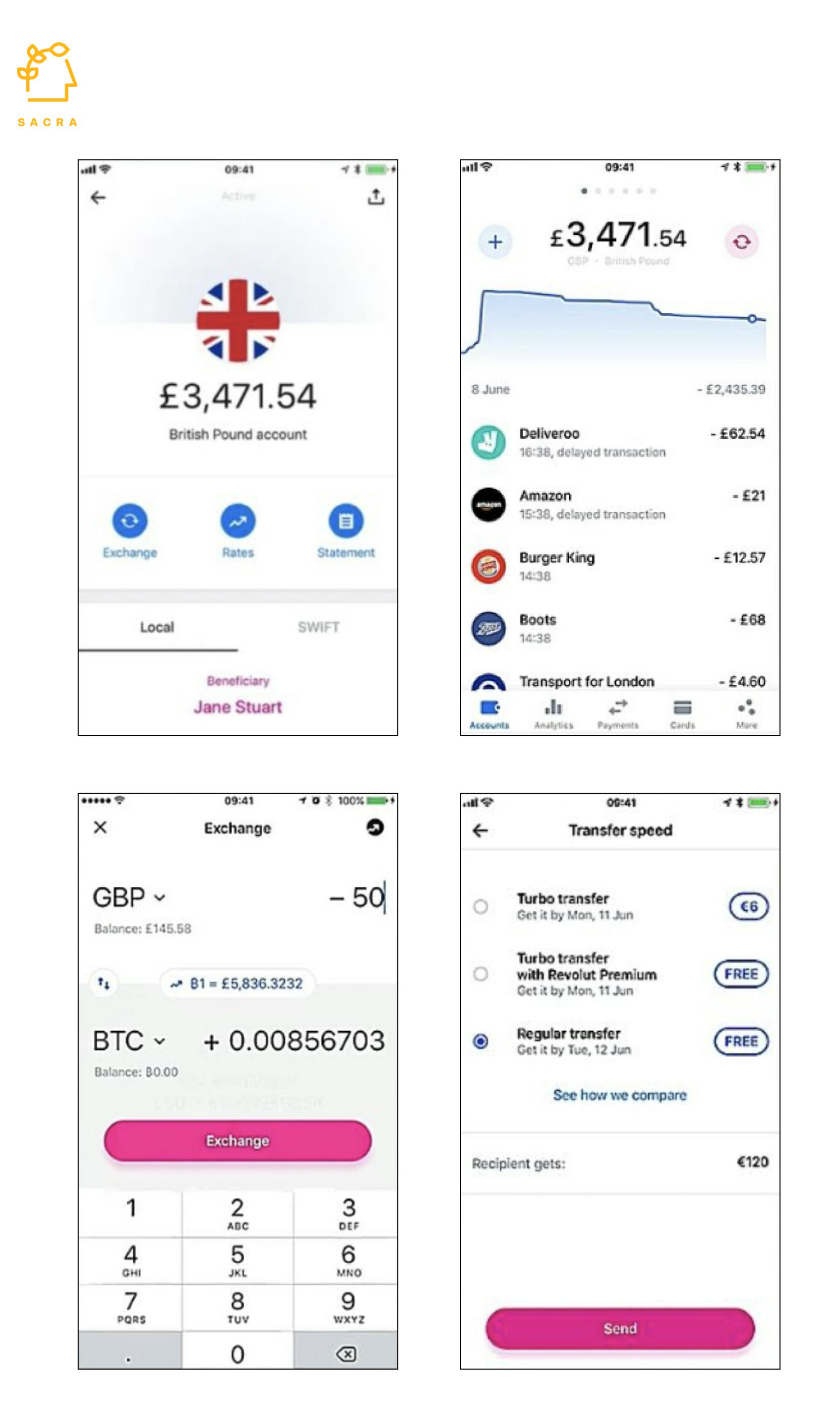

Revolut has 4 primary revenue streams:

- Cards and interchange revenue when customers use their debit cards for purchases

- Subscription fees from paid plans that unlock more benefits for business and retail customers

- Forex revenue charged as a markup or a fee when customers make foreign currency transactions

- Wealth comprises revenue from cryptocurrency, commodities, trading, and savings products

Revolut generates more than three-fourths of its income from cards and interchange, and paid subscription plans. In 2020, while the interchange revenue’s growth was slow, it was partially offset by the ~100% YoY growth in subscription revenue.

Business Model

Revolut is building a destination for a user’s all financial needs, like the Chinese super apps WeChat and AliPay, by expanding globally and adding more features to its original forex card proposition. Unlike its competitors, Revolut opted not to apply for a banking license early, making it faster and cheaper to grow with less regulatory pressure. Revolut releases new features rapidly, such as metal cards, cryptocurrency, stock trading, travel insurance, bill splitting, and a consumer-friendly mobile banking experience. It is also branching out geographically in an Uber-like manner to 36 countries, including the US, Australia, Singapore, and India while localizing and translating its app to conform to different regulatory and customer contexts.

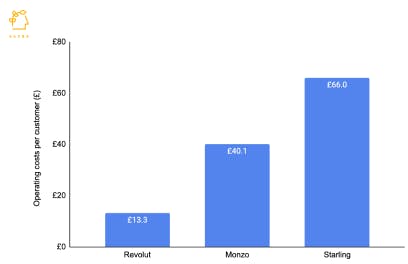

As Revolut grows, it is eating up more financial transactions for more customers and monetizing them through transaction fees. At £95.4M, its interchange revenue exceeds its competitors, such as Monzo and Starling Bank. The expansion comes at a cost, and its operating costs grew 2x in 2020 to £266M, but due to its large customer base, Revolut’s per-customer operating cost is the lowest among UK neobanks.

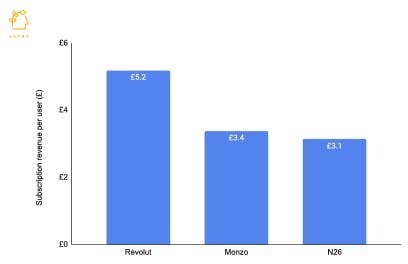

Its rapid product velocity also helps it upgrade more customers to paid tiers as its subscription revenue grew 5.5X to £75.2M in just two years. Revolut is more efficient in upgrading users to paid plans, with per-user subscription revenue being the highest among the large neobanks in Europe. It offers three retail plans at monthly fees of £2.99, £6.99, and £12.99, and three business banking plans at £25, £100, and custom pricing for large customers. Revolut’s sales and BD headcount driving the paid subscription push grew over 150% in the last 12 months, reaching one-fourth of its workforce, much higher than other neobanks. It also launched a new paid tier at £2.99 per month, the cheapest plan among all European neobanks.

Product

Revolut found an initial product-market fit by offering a prepaid forex card with lower transaction fees than the legacy banks, making it popular with young digitally-native travelers. Later Revolut bolted on more products that this demographic found useful to offer them more than just a forex card.

Revolut has a banking license for the EU and offers different products in different countries depending on its banking license and local regulations. Its products can be categorized into retail banking and business banking.

Retail banking has everyday banking products, investments, and travel & forex.

- Investments: Crypto, stock and commodities trading, and interest-bearing saving accounts.

- Travel & forex: International remittances, currency exchange, and hotel booking.

Business banking has cards and accounts, payments, treasury, and SaaS.

- Cards and accounts: Employee debit cards, virtual cards, multi-currency accounts.

- Payments: Send and receive payments in multiple currencies, payment links, and payment gateway.

- Treasury: Fx forwards and crypto trading for businesses.

- SaaS: Business spend management, digital invoicing, and integration with apps like Xero, QuickBooks, and Sage.

Competition

Revolut is the largest neobank in Europe with 20M customers, compared to 7M of N26, 5.8M of Monzo, and 2M of Starling Bank. While Monzo positions itself as the everyday bank for everyone, Starling focuses on B2B banking and selling BaaS to fintech, and Revolut and N26 have focused on geographic expansion. Revolut offers more features than its competitors, such as crypto, stock trading, and a lower-priced plan.

Even though Revolut is larger than its neobank peers in Europe, it’s not the largest bank in the key markets. The UK, France, and Germany account for over half of the total banking market in Europe by asset size, and Revolut is not the leading neobank in any of them. Another challenge for Revolut is that, unlike its peers, Revolut operates as an e-money company, which means it can’t offer checking accounts or state-insured deposits. Most importantly, it impacts its business banking product as it cannot offer loans or working capital advances to SMBs, one of their key business needs.

Another challenge for Revolut is that customers use it as their secondary account and traditional banks for primary accounts. This reflects in its average customer deposit of £317, compared to £15,900 for Lloyds and £25,000 for Natwest.

TAM Expansion

Revolut’s TAM expansion approach is to continue to expand to more geographies and cover more financial transactions for its customers. It aims to be present in 90 countries in 2022, entering new countries by offering a forex app that’s core to its origin and then ramping up its services. However, it considers getting banking licenses in the UK and the US as the critical drivers for future growth.

It has started offering credit products such as personal loans in select markets, making it more valuable for its users. It is also launching features beyond core banking, such as ‘Stays,’ which allows users to book travel accommodations within Revolut’s app for cashbacks, and Shopper, a Honey-like browser extension to find and automatically apply discount codes while shopping.

Risks

US and UK expansion

Disclaimers

This report is for information purposes only and is not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal trade recommendation to you.

Information and opinions presented in the sections of the report were obtained or derived from sources Sacra believes are reliable, but Sacra makes no representation as to their accuracy or completeness. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a determination at its original date of publication by Sacra and are subject to change without notice.

Sacra accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to Sacra. Sacra may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect different assumptions, views and analytical methods of the analysts who prepared them and Sacra is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report.

All rights reserved. All material presented in this report, unless specifically indicated otherwise is under copyright to Sacra. Sacra reserves any and all intellectual property rights in the report. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of Sacra. Any modification, copying, displaying, distributing, transmitting, publishing, licensing, creating derivative works from, or selling any report is strictly prohibited. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Sacra. Any unauthorized duplication, redistribution or disclosure of this report will result in prosecution.